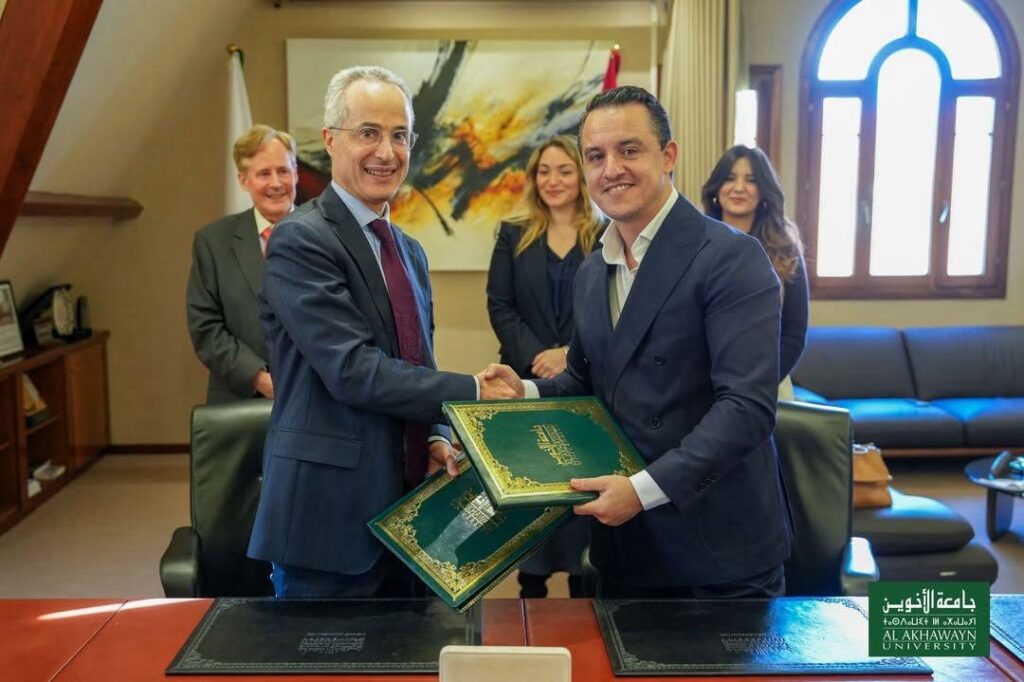

Ifrane – Mr. Ahmed Abbad El Andaloussi, Founder and CEO of Lotus Capital Gestion, and

Mr. Amine Bensaid, President of Al Akhawayn University, signed a partnership on November 21,

2024, marking the launch of the « Executive Trading Certificate. »

This certificate, developed by Lotus Capital

Academy and Al Akhawayn University, is a

program that places the highest academic

and professional standards at its core. It

offers training aligned with the latest market

requirements and covers a broad spectrum

of fundamental concepts, including

algorithmic and quantitative trading.